Retrospect and Prospect of Financial POS Machine Industry Development

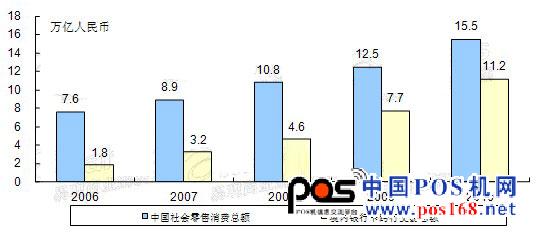

Figure 2006-2010 China's total social retail consumption, total domestic bank card inter-bank transactions

Source: National Bureau of Statistics, People's Bank of China, 2011

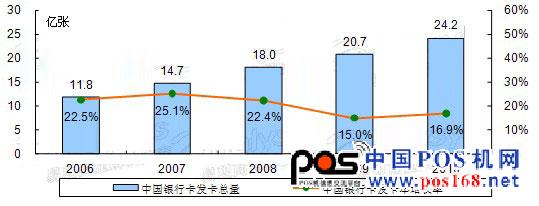

As of the end of 2010, the total number of bank card issuance in China was 2.42 billion, an increase of 350 million compared with the end of 2009. The popularity and deepening of card consumption has become the driving force behind the development of the financial pos machine industry. The growth of the number of bank cards and the amount of bank card transactions has directly led to the rapid development of China's financial POS machines. The market application of financial POS machines has been expanding, bank cards. The payment environment has been greatly improved.

Figure 2006-2010 China Bank Card Issuance and Annual Growth Rate

Source: People's Bank of China 2011

China's financial POS machine industry has briefly adjusted in 2009 and then entered the fast lane of development. The increase in the number of bank cards and the amount of bank card transactions directly led to the rapid development of China's financial POS machines. The market application of financial POS machines continued to expand, and the bank card payment environment was greatly improved. In 2006-2010, the CAGR of China's financial POS machine sales reached 44%, and the market developed rapidly. Especially in 2007-2008, China's financial POS machine industry experienced sustained ultra-high-speed development (about 60%), which made the financial POS machine market relatively large and the market development normative; in 2009, China's financial POS machine market entered During the short adjustment period, the growth rate has slowed down, but the growth rate reached 40% in 2010. With the launch and vigorous development of emerging markets (such as the contactless card payment terminal market and mobile payment terminal market) in recent years, the future POS machine The market will face a new round of prosperity. The chart below shows the development of China's financial POS machines in the past five years from the scale of sales and the scale of sales.

Figure 2006-2010 China Financial POS Machine Sales Scale

Financial POS machine industry concentration is strengthened, domestic enterprises lead the market

The market competition in the financial POS industry has undergone great changes: market concentration has increased significantly, market participants have become increasingly concentrated; Chinese companies have dominated most of the market with absolute advantage. After years of market evolution, the market has been reduced from the early dozens of POS vendors to the competition between several large domestic and foreign manufacturers. The concentration of the industry has increased significantly, showing a monopolistic competitive market characteristics; the future competition will be more intense. Industry concentration has further increased. In the market competition, Chinese companies broke the situation that initially monopolized the market by large foreign companies. At present, Chinese companies have no big gaps in technology research and development, product quality and performance with large foreign companies. On the contrary, Chinese companies are superior in terms of customer development, service network and service quality, thus occupying a larger market. Share, in 2010, Chinese companies accounted for more than 70% of the domestic financial POS market.

Product prices are lower and competition content changes

After years of full market competition, the price of financial POS machines has dropped significantly. In the initial stage of the financial POS machine industry, foreign large enterprises have formed a situation in which the product price is extremely high due to its strong monopoly position. Due to the low barriers to entry of financial POS machines, the industry is lucrative and attracts more companies to participate in market competition. This will inevitably lead to intensified market competition, the emergence of price wars, and the final product price return to rationality. At present, the average market price of a single ordinary financial POS has been reduced from the price of nearly 10,000 yuan a dozen years ago to about 1-2K. .

The result of shuffling in the industry has changed the connotation of market competition. The weaker enterprises have been eliminated by the market, and the remaining enterprises have been unable to win in the market by relying solely on price wars. The connotation of competition has turned into a contest of comprehensive strength of enterprises. Deeper competition in design, brand, quality, technology, service, marketing network, etc., brings higher requirements and greater challenges to enterprises.

The second-tier cities and rural areas will be the highlight of market development under the policy

The development of China's financial payment environment is uneven, which makes the financial environment of the second-tier cities and rural areas seriously lag behind the development of big cities. With the in-depth development of China's economy, the small and medium-sized merchants in the second-tier cities and rural areas The demand for the use of bank cards is getting stronger and stronger, and it basically has the conditional basis for the promotion and popularization of bank cards. Therefore, under the joint effect of various factors, the second-tier cities and rural areas will usher in an accelerated construction period of the financial payment environment.

At the end of 2008, the State Council specifically mentioned the requirement of “further promoting the use of bank cards†in the “Opinions on Invigorating Circulation and Expanding Consumptionâ€; the People’s Bank of China also announced on July 16 the “Guidance on Improving the Payment Service Environment in Rural Areasâ€. For the first time, the guiding ideology, overall goals and specific measures for the construction of “payment service environment in rural areas†were clearly put forward. The overall target requires that by 2012, the number of cards per capita in rural areas will be one, the proportion of card consumption in social retail goods will reach 10%; the number of ATMs and POS machines in rural areas will reach 60,000 respectively. With 240,000 units, merchants accepting bank cards increased by 10%, and ATMs and POS machines were deployed in a poorer county.

The emerging payment terminal market will contain huge market opportunities

After many years of rapid growth, the traditional financial POS market has a large market stock and has been developing steadily, so the market development space is limited. The emerging payment terminal market segment: the non-contact card payment terminal market and the mobile payment terminal market are in the start-up period, which contains huge market opportunities. At present, these two areas have not yet undergone large-scale market operation, but the future development potential is huge. In particular, the development of the mobile payment field is eye-catching, and is supported by China's huge mobile phone user base, the maturity of mobile payment technology and the popularity of 3G, the national policy support for mobile payment, and the strong promotion of mobile operators by mobile operators and UnionPay. Under the comprehensive promotion of factors, the future development has a "blowout" trend. At present, the mobile phone payment of UnionPay has completed its preliminary layout, and more than 100 local banking institutions in 10 provinces and municipalities across the country have already carried out related business. UnionPay plans to complete more than 700,000 retail POS machines in 2011 to support mobile payment services and provide consumers with better payment channels.

- 100% sugarcane fiber: The bagasse plate is made of 100% sugarcane fiber, a sustainable, renewable, and biodegradable material. A great alternative to traditional paper or plastic, The disposable plate offers the same sturdy function and easy cleanup, yet it`s completely tree- and plastic-free.

- 100% compostable: since it`s made from 100% sugarcane fiber, The plate can be commercially composted (no need to send it to a landfill). the plate offers a disposable design that will degrade quickly, which means convenient cleanup for you, your customers, and the planet.

- Hot or cold use: these plates can be used for hot or cold food items. It offers reliable strength and does not contain any plastic or wax lining. These plates are microwavable & freezable. Oil and cut-resistant note: hot foods can cause the plates to perspire and condensation to form at the bottom.

- Perfect for any occasion: with a wide range of products and a classic design, Stack Man provides premium environmental -friendly products and Peace of mind that you are providing all-natural organic tableware for your family and friends. Perfect for camping, picnics, lunches, catering, BBQs, events, parties, weddings and restaurants.

Sugarcane Bagasse Plate,Sugarcane Plates,Biodegradable Thali Plates,Wholesale Compostable Plates

Guangxi U-Yee Environmental Technology Co.,Ltd , https://www.biodegradetableware.com